For long-term investments, I look for businesses that operate on high margin, produce high investment return, generate a lot of cash, and trade at attractive valuation. The recent IPO of Chinese online gaming company Giant Interactive (GA) is one that I find meets all of these conditions.

GA is a three-year-old company and a newcomer to the Chinese online gaming industry, specializing in MMORPGs (Massively Multiplayer Online Role-Playing Games). Its first MMO game, ZT Online, went into commercialization only in January 2006. The game established Giant as an industry leader, as ZT Online was rated the most popular online game in China in the same year by both IDC and game players.

GA is a three-year-old company and a newcomer to the Chinese online gaming industry, specializing in MMORPGs (Massively Multiplayer Online Role-Playing Games). Its first MMO game, ZT Online, went into commercialization only in January 2006. The game established Giant as an industry leader, as ZT Online was rated the most popular online game in China in the same year by both IDC and game players.

ZT Online’s great start presented itself well in the company’s financial performance. Its first six months (following commercial launch) brought in RMB 82.4M revenue and 43.5M net income. Each of the following two six-month periods recorded three-digit sequential growth. Revenue for the second six-month period (ending December 2006) increased by 296% sequentially to RMB 326.1M and net income increased by 362% sequentially to 201.1M. Then the third six-month period (ending June 2007) saw sequential revenue growth of 111% to RMB 687.5M and sequential net income growth of 155% to RMB 512.3M.

Obviously this type of growth rate is not sustainable. So Q3 began to revert to the more normal sequential growth rates. In the quarter net revenue grew by 9.5% sequentially and net income grew by 9.8% sequentially over Q2 of the year. The abrupt growth deceleration appears related to the life cycle of MOM games which tend to peak roughly 18 months following commercial launch.

The peak out of ZT Online is hardly a secret. But the abruptness of the growth deceleration has caught the street by surprise. Shares of GA plummeted by 25.4% on Nov.20, the day Q3 results were announced. The drop from the previous day’s intraday high to the day’s intraday low was even more spectacular, at 41.1%.

The street’s naivete and irrational speculation can mean a great opportunity for rational investors. The challenge is of course to identify true winners. GA appears to be a clear winner by the criteria stated at the beginning of this article.

Being a high-tech service company and in the lucrative online gaming industry, the company enjoyed exceptional profit margins. For 2006, gross margin was 88.9%, operating margin 59.6%, and net margin 59.9%. For the first nine months of 2007, gross margin was 89.7%, operating margin 73.3%, and net margin 73.4%. Net income and margin were helped by the company’s current tax-exemption status (total exemption for 2006 and 2007; 50% reduction from regular tax rate of 15% as a high tech company, or 7.5%, 2008 through 2010).

Being a high-tech service company and in the lucrative online gaming industry, the company enjoyed exceptional profit margins. For 2006, gross margin was 88.9%, operating margin 59.6%, and net margin 59.9%. For the first nine months of 2007, gross margin was 89.7%, operating margin 73.3%, and net margin 73.4%. Net income and margin were helped by the company’s current tax-exemption status (total exemption for 2006 and 2007; 50% reduction from regular tax rate of 15% as a high tech company, or 7.5%, 2008 through 2010).

Since China is implementing a new tax law, starting 2011 the company might be paying either 15% or 25% income tax (not clear yet). At the more stringent regular tax rate of 25%, NOPAT (net operating profit after tax) margin for FY 2006 and first nine months of 2007 were 44.7% and 55.0%, respectively. This means that the company would still have pocketed $0.45 and $0.55 of net profit for each dollar of sales it had made in FY 06 and first nine months of 2007, respectively, had it been taxed at the hypothetical 25% tax rate.

Seasoned investors understand that great earnings do not always translate into great cash flows. A common cash-flow problem is caused by growing accounts receivables. GA certainly does not fall into this category. Game players prepay for virtual products and services offered in its online MMO games (currently mainly ZT Online). Not only are there no accounts receivables to worry about, but also does the company collect deferred revenues (prepayment for game cards and game points) which accumulate to operating cash flow immediately.

As such, GA’s cash flow from operations actually surpasses net income. In addition, the company’s free cash flow has surpassed net earnings as well, due to relatively moderate capital expenditures.

Cash was accumulated so fast that at the end of 2006 and Q3 2007 it significantly surpassed the shareholders’ equity. Cash was so plentiful that about RMB 900M was advanced to finance CEO Mr. Shi Yuzhu’s other business (Shanghai Jiante) in Q1 and Q2. Without such cash advances, Q1 and Q2 07 would also have registered cash and equivalents that significantly surpass total shareholders’ equity. During Q&A session of the Q3 conference call, CFO Mr. Eric He boasted about having plentiful operating cash flow onshore that they can afford to leave the IPO proceeds offshore in a U.S. account for the time being.

That fast-participating cash along with no debt (who needs that with so much cash) makes invested capital (which involves taking away cash and adding debt to equity) appear virtually non-existent. In other words, the ROIC (return on invested capital) appears astronomically high, making the management seem magicians who can turn air into gold.

An alternative measure of investment return is ROE (return on equity). For the one-year period [TTM] ending September 30 2007, I have used the average of year end 2006 and Q3 2007 as an approximation of equity (out of lack of balance sheet data for Q3 06) which is RMB 616.9M. And again I have stripped off the positive impact from the company’s current tax-exemption status by using NOPAT at the hypothetical 25% tax rate, which is $664.9M. These translate into an ROE of 108% for the one-year period ending September 30 2007.

Of course, with the immense IPO cash proceeds the ROE will no longer remain at this level. My estimate for FY 07’s ROE, using average equity for the year and NOPAT at the hypothetical 25% tax rate, is about 23%. The corresponding estimate using FY 07’s net profit (derived from the company’s low revenue projection for Q4) is about 31%. Again note these are the returns when the entire equity is virtually cash. Presently the company has about RMB 6.8B of cash (including both cash generated from operation and the IPO proceeds).

Technically speaking ROE is not as insightful a measure as ROIC. But in GA’s case where ROIC is ridiculously high ROE gives us an alternative way to see the exceptional return the company generated while still virtually hoarding all its equity as cash in the bank. As such, the company is simply in a great position to expand its business and withstand any downturn.

GA's solid cash position also means that, in the intermediate term, it will not have to pursue additional financing (like issuing bonds, secondary public offering, etc.) that could have a negative impact on the share price.

To value this company, I used a DCF model with 16% discount rate. Here are the assumptions I made: (1) the company will be in business for the next 30 years only, (2) free cash flow [FCF] is equal to net earnings, (3) the company will grow FCF or earnings at 27% annual rate for the first five years (starting 08), followed by 15% for the next five years and 7% for the remaining 20 years. I arrived at $12.30 (per share) when I used the hypothetical (25% tax rate) NOPAT for this year, and $16.32 (per share) when I used an estimated net earnings for FY 07. So this model puts the stock at $12.30 to $16.32 per share.

It should be obvious that this model used largely conservative estimates. Particularly, the 16% discount rate used was quite stringent. Moreover, the initial growth rate was assumed to be below some analyst’s forecast of 30 to 40% revenue growth rate for the Chinese online gaming industry as a whole in the next few years. According to iResarch, the industrial revenue in 2006 grew 60% over 2005. And it reached RMB 3.04B in Q3 2007 alone, compared to RMB 7.68B for whole year 2006. As of Q3 GA's market share was third in the industry, at 13.8%, only trailing NetEase's (NTES) 15.1% and Shanda's (SNDA) 18.4%.

If you have not followed this company, you could be wondering where the growth comes from, given ZT Online has likely peaked. The answer is GA certainly is not a one-trick pony. The company's second online game, Giant Online (a 2.5D MMO game) is in closed beta testing and has already attracted thousands of players. Based on data collected from the beta testing, Mr. Shi expects this game to generate at least the same level of revenue as ZT Onlne. Furthermore, the company will be rolling out its licensed 3D game King of Kings III next year. And you can count on more games to be developed and released in the future.

Investing in GA is more or less capitalizing on CEO Mr. Shi Yuzhu’s past success and failure. Mr. Shi is a high-profile entrepreneur in China. As early as 1993, his software company Zhuhai Giant Group was the second largest private enterprise in China. In 1995 he was ranked 8th on Forbe’s first-ever China rich list. In the mid 1990s, Zhuhai Giant even received the attention and visits from China’s top leaders like Li Peng (former Premier), Hu Jintao (current President), and Zhu Rongji (former Premier). Mr. Li Peng (then Premier) was reported to have visited Zhuhai Giant once a year during that period.

Unfortunately, Mr. Shi’s enterprise collapsed around 1997 due to over-ambitious business expansion, real estates speculation, and disregard of fundamental business principles. Mr. Shi’s fall became one of the most famous in China’s modern enterprise history.

But Mr. Shi proved that he can learn and benefit from failure, even a major one. In early 2000s Mr. Shi reemerged with great strength through successful healthcare and nutrition businesses (Shanghai Jiante, etc.) and equity investment (Giant Investment, etc.). That enabled him to venture into the lucrative online gaming industry in late 2004. In just a year, his first MMO product ZT Online hit the market with great success.

Other than Mr. Shi’s well known marketing acumen, it appears there are two other key elements that have helped Mr. Shi to reemerge and will empower him for a lasting success. One element Mr. Shi learned from his Zhuhai Giant collapse, i.e., cash position and liquidity is the life of enterprise. The other element he discovered in his previous success and it is called high margin businesses. Mr. Shi does not believe in low-margin high-volume businesses. He thinks the way to business success is to focus on high-margin areas.

And so far we have seen GA’s enormous cash-generating power and high profit margins to be well aligned with Mr. Shi’s philosophy.

Mr. Shi understands the online gaming industry by being a regular game player himself. Even before he founded Shanghai Zhengtu, he had acquired unique insight into virtual products, absentee role-experience-level boost, external game-cheating programs, etc. Some credited him with being the first to introduce the free-to-play business model into China, even though Shanda was officially the first to announce it. It was said that one of Zhengtu's vice presidents had accidentally let out Mr. Shi's idea to Shanda. Mr. Shi's gaming industry insight will continue to be a key contributor to GA's success.

Mr. Shi is also a close friend of China's business heavy-weights like Mr. Duan Youngji (Co-founder, CEO and Chairman of Stone Group) and Liu Chuanzhi (Co-founder, former CEO and Chairman of Lenovo). Mr. Duan and Liu were Mr. Shi's coaches even during his most difficult times.

Most of GA’s current senior management (President Liu Wei, COO Zhang Lu, and vice presidents) has at least worked with Mr. Shi either since Zhuhai Giant or Shanghai Jiante. Mr. Shi thinks the great fall that he and his team have been through together is his most precious asset. Along with the lessons learned from the previous notorious failure, this loyal management team has full knowledge and thorough understanding of Mr. Shi’s unique marketing methodology and operational philosophy.

GA’s CFO Mr. Eric He is a Wharton School MBA and CPA and Chartered Financial Analyst in the U.S. He has quite extensive financial career background. It is clear from Q3 conference call that Mr. He stands out among the CFOs of young Chinese companies in terms of communication with U.S. analysts.

Enough good has been said about this company. Now I do want to throw in a few chilling words of caution.

Firstly, the lucrative online gaming industry is also where the best young Chinese entrepreneurs are. Mr. Shi is competing with the likes of Mr. Ding Lei (NetEase) and Mr. Chen Tianqiao (Shanda). GA still has a great catch-up to do to capture the top spot. We have seen a great start. But whether Mr. Shi and his team can keep the momentum going remains to be seen. If Mr. Chen Tianqiao is right, however, the online gaming industry is growing fast and has room for multiple players to coexist and grow together.

Secondly, the insiders have too much power by owning the majority stake of the company. Following the IPO, the senior officers own 57.22% of the company. Forgive me for not mentioning the benefit of insider ownership.

Thirdly, the prepayment business gives the management a lot of room to manipulate the deferred revenues. Quarters can be easily made stronger or weaker than they actually are. For example, given the precipitous drop in sequential growth in Q3, could Q1 and Q2 have been dressed up at the expense of Q3 and Q4 to boost IPO performance?

No, I’m not suggesting they have done that. It is my hope the management has not taken and will never take advantage of the deferred revenues to dress up or down quarterly or annual financial performance. A truly smart management will never do that. After all, they are supposed to follow GAAP. But if they are truly brilliant, they should have learned from the recent class action lawsuits filed against them.

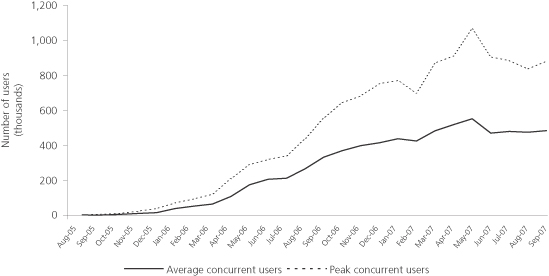

GA's prospectus disclosed (p.1) PCU and ACU of 888,146 and 481,054, respectively, for Q3 2007. It also included a chart (p.94, click here to view) that plots monthly ACU and PCU versus time through September 07. PCU and ACU decline can be seen starting in June and lasting into Q3. The prospectus also attributed the decline to game rule changes. Still, it has not prevented law firms from alleging failure of disclosure on declining ACU and PCU in Q3.

{kind=link}

The management should understand that cash-rich companies make perfect target for class action suits. So it has no choice other than remaining fully honest and transparent when it comes to financial disclosure. After all, it is quite dramatic for a company to be in class action suits less than a month after going public.