Recent World Events Are Bullish for Metals

I noticed a few important world events happened in the last 24 to 48 hours and triggered dramatic rallies of a few related metals, including palladium, platinum, nickel and aluminum. Let me discuss those events.

First, something that must be described as a paradigm shift event in the palladium market. No one noticed this Bloomberg news except for a few fast thinkers, who immediately responded. Palladium price instant jumped up $12. But more spectacular is the spike in the palladium lease rate. I have NEVER seen such a big lease rate spike in any precious metal! Please read this to understand the significance of metal leasing rate.

Quote from the news:

The metal (palladium) rallied after Russia's OAO GMK Norilsk Nickel, the world's biggest producer, said its stockpiles of the metal may be "depleted'' in one to five years as the government reduces its holdings.

One to five years? Why such a big margin of uncertainty? I think they are really explicitly saying it's zero years, there is virtually no more government palladium stockpile left. This is a gigantic paradigm shift event that palladium investors have been waiting for for years, and that many speculate it is getting closer, the depletion of Russian palladium stockpile. This is a paradigm shift because over past years, massive Russian stockpile palladium sales, up to the tune of 2 million ounces per year, was the reason that the Pd market was in surplus. But the stockpile has to be depleted one day, and when it happens, the palladium market shifts from structural surplus to a large structural deficit, which is extremely bullish. Some strong-hand investors have been waiting for this since 2003, as I discussed before , and looked at again recently. Read today's mineweb piece: The Russian palladium stockpile - do we need to worry?

A second event that just happened is also very significant.

Nickel rallied strongly up 6%+ on Thursday, as investors now believe nickel is in supply shortage again, rather than surplus. This is caused by the supply disruption due to the big natural gas blow up in western Australia. But more importantly, BHP announced that it shuts down the Kalgoorlie smelter for at least four month, removing 2% worth of the world's nickel supply. This news is quite bullish for nickel.

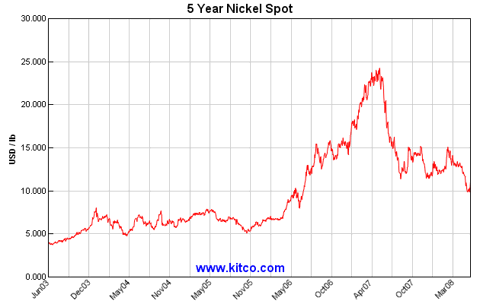

Third event came from China. A whole batch of nickel producers in China are shutting down production. During the strong nickel rally which peaked at $50/kg in May 2007, a number of producers of the so called nickel pig iron emerged. The nickel pig iron production process is highly pollutive, energy intensive and costly but was profitable at $50/kg nickel price. As nickel pig iron flooded the market, nickel price now drops to an unprofitable level for these producers. On top of that, electricity tariff has been increased by 170%. The higher cost forces producers to shut down. Another reason is China is preparing for the Summer Olympics and so a whole lot of air polluting industries were ordered to shut down in order to clean the air pollution. As a result, now traders widely believe that the nickel market has turned around to supply shortage again and price must surge.

{kind=link}

The year 2008 , China Olympics Year , is a pretty big deal in China. The folks consider the number 2008 , which ends with an 8 , a lucky number, on top of it, Olympics is first held in China. So there are lots of jewelry and souvenir buyings and lots of young Chinese couples are getting married this year, boosting demand on precious metal wedding bands. This development is bullish for both PGM metals, palladium and platinum, as I talked before.

But the most important development as far as PGM metals are concerned, of course is the PGM production disruption in South Africa, due to the on-going and long lasting electricity crisis there. Many people noticed the headline on January 25, 2008, and then soon forgot about it and assumed that everything is back to normal again in South Africa. The electricity supply there is far from normal and it is actually getting worse, and more bad news from ESKOM is revealed as days go by. I often visit the ESKOM web site and click on the Media Rooms->News on ESKOM link. So I keep track of things happening there.

ESKOM now claims that the electricity crisis will last at least seven more years. After tracking the news and analyzing the data from ESKOM, I draw the conclusion that the South African electricity crisis is more than just a problem of outdated facilities and lack of electricity generation capacity, but a coal supply problem as well. Most importantly it is a money problem. And sealing it all, it is a problem of lack of leadership and lack of vision, not just in ESKOM, but in South Africa Government, and even within the people of South Africa.

Money buys you things and pretty much fixes everything. ESKOM could get new electricity capacity built and coal supply secured, on a fast track, to fix the electricity supply problem, IF it had the money. But it does NOT have the money. It is broken, bankrupt! That's a fundamental problem. With money, most everything can be solved. Without money, nothing can be fixed.

It's a problem when you run a country on socialist principles instead of on free market. South Africans pay the lowest electricity tariff in the world when energy cost is skyrocketing: 11 cents per KWH for foreign customers, 17 cents for domestic industry, and 41 cents for households. That's in South African Rand. Divide it by 8.1 to convert to US$. It cost far more for ESKOM to generate the electricity than it gets paid.

Let's look at ESKOM's 2007 Financial Report. Electricity tariffs collected was R40.068B (US$4.95B). Cost to acquire fuels, namely coal, natural gas, diesel and uranium, was R13.040B. ESKOM distributed 241.170 billion KWH of electricity in 2007. So average tariff was R0.166, or US$0.0205 per KWH. I think we in America are now paying up to 25 cents per KWH! Using the energy equivalence calculator, and use quoted energy efficiency of about 35% of SA power plants and that they use the low quality coal (lignite), it costs about 0.59 kilograms of coal to generate one KWH of electricity. So they burned roughly 143 million tons of coal in 2007, roughly nearly half million ton per day.

And it cost ESKOM only R13.040B to acquire the coal and other fuels? That's only R91.20 per metric ton of coal, or US$11.26 per metric ton. Where did ESKOM get coal so cheap? Where can ESKOM continue to get such cheap coal? Internationa coal price is now approaching $160 per metric ton . The Indians are happily coming to South African harbors and pay well over US$100/ton thermal coal at free on board basis. I am quoting this , which is just hilarious:

I think it just reflected poorly on Eskom in terms of their coal purchasing. After the mining indaba in Cape Town in February it was quite amazing - we were flying in to have a look at the Camden Power Station with two to three days supply in front of it, and it just so happened that at the time there was a train with 200 wagons of export quality thermal coal chuffing past.

Clearly ESKOM doesn't have the money , and can't compete with foreign customers for South Africa's coal. I can not believe they paid

US$11.26

per ton. Using trucks to transport coals to the power plants would cost more than that, even if they get the coal for free from mines. The root of problem is South Africans are paying too little for electricity. That's the whole reason ESKOM wants an immediate 53% tariff increase. But every one said NO and Mboweni wants only 6% electricity tariff increase , and the labor union is planning a massive strike against the electricity tariff increase.

With no hope of dramatic increase of tariff income, ESKOM must borrow money to fill the hole of coal cost. But who would lend knowing they can't pay back? South Africa, with double digit inflation rate, above 35% unemployment, and people impossible to accept a 53% increase of a super cheap electricity tariff, is a broken system with broken leadership, and there is no hope of fixing the electricity crisis any time soon. With winter approaching, it's almost guaranteed they will run into another round of deep electricity supply crisis, disrupting mine productions, including PGM mines.

It's important for people to pay attention to what's happening in South Africa, because PGM supply shortfall there provides a virtually guaranteed bullish case for palladium and platinum. That turns North America's only two PGM mining companies, North American Palladium (PAL) and Stillwater Mining (SWC) , into extremely excellent investment opportunity, with high reward virtually guaranteed in the near future.

The recent nickel rebounce further strengthens the bullish case for PAL, who produces nickel as a significant byproduct. I am also trying to look for other cheap nickel players. Norilsk Nickel (NILSY) has fallen down from recent high but it is not cheap at all. I noticed that FNX Mining (FNXMF.PK) has recently been added to the naked short list . The price seems to be at a low level. I need to spend more time research it. But many times, stocks on naked short list may rally strongly on ensuring short squeezes. One example is LDK 's rally from its recent lows in March. I noticed there was heavy naked short going on on LDK at that time, so I curiously watched and surely it put up some nice rally when the nakes shorts covered.

Someone asked about aluminum stocks. Many aluminum stocks had been red hot and have since fallen from their recent highs, like AA, ACH, CENX, KALU, NX , SPSX, and TG. All of them have fallen down, even though aluminum price is still near its historical high. Why? Are these aluminum stocks at a good price to buy?

ACH caught my attention in mid August, 2007. I watched it rally from $40 to $80, but I wasn't impressed at all and never thought about buying it, now ACH is right back to below $40.

The reason I never got interested in aluminum is that as a natural resource investor, I know aluminum is a virtually unlimited natural resource. You could never exhaust the aluminum mineral reserve of the world. Production of aluminum is just a matter of transporting the raw material, and then producing it using electricity. When the supply is tight, anyone can spend some money and set up a shop to process aluminum, so the competition diminishes profit margin. And then skyrocketing energy cost really cuts into the corner of any aluminum producers. That's why I could never become interested in any aluminum player.

For any natural resource player, you need to look into the basic economic fundamentals of supply and demand. Look at where the raw material comes from. Is it scarce or abundant? What's the cost of processing it. Also look at the demand side, is it price elastic or inelastic?

Using these principles, I am not too big a fan of coal. I really liked JRCC and bought it at $4 a share only because I found the share price incredibly low, the price/sales ratio was incredibly low, and the quarterly loss was only a small fraction of the sales revenue, and I knew coal price has got to go up. But coal price has gone up too far, too fast and I do not think it can last. Nowadays you can not go to a financial web site without seeing names of coal mining companies being mentioned by every one, like PCX, ACI, APA, BTU, JOYG.

If everyone is talking about coal stocks, that sounds a bit like a bubble. the world still has plenty of coal reserves left. According to a recent BP survey of global coal production, consumption and reserve, global coal supply/demand is roughly in balance. The shortage is no more than 1%. So any disruption is local and temporary in nature. Recent coal price raise of double or even triple is not warranted by the supply/demand relationship and could be in large part attributed to speculator bidding price up.

My advice is it may be time to sell your coal stocks before they reach the top. Move on to something else. don't try to catch the very top, which few people can do. I would think natural gas is way much better than coal. Natural gas is limited, depleting faster than oil, and is less talked about than oil. have a look at natural gas stocks like CHK, SWN, CNP, NGAS, NFX, WMB.

The Atlantic hurricane season is coming and natural gas may get a boost if this hurricane season is relatively active and may hit some platiforms in the Mexican gulf.

But I think nothing beats the scarcity and price inflexibility of PGM metals, platinum, palladium, rhodium, the narrow playing field (only PAL and SWC in North America), and the lack of mentioning of these two stocks in the investment community. Plus isn't it true that South Africa's winter is fast approaching and will come earlier than the first Atlantic hurricane?

So I am sticking with my PGM plays, SWC and PAL, and will only consider putting small stakes in natural gas fund UNG, and a few select natural gas stocks.