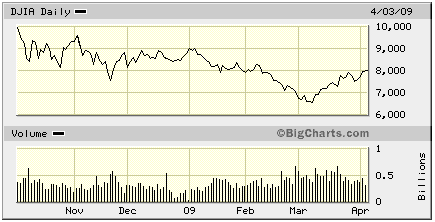

Is This a Sucker Rally or New Bull Market?

It has been quite a month.

The newspapers were full of stories last week about how March was the best month for stock markets in six years and that the last four weeks were the best stretch for equities since either 1933 or 1938, depending upon the source.

The distinction is unimportant as investors have gotten the message - stocks are on a tear: Broad indexes have risen between 20 and 30 percent over the last month and recent reports have shown a deceleration in the rate of decline for some economic indicators and tentative signs of a bottom for others, leading many to believe that the worst is now behind us.

Broad indexes have risen between 20 and 30 percent over the last month and recent reports have shown a deceleration in the rate of decline for some economic indicators and tentative signs of a bottom for others, leading many to believe that the worst is now behind us.

The move up in equity markets since the early-March low has officially entered "bull market" territory after a flurry of government actions, pronouncements of profitability from Wall Street firms, and optimism that global leaders at the G20 meeting are taking steps to tackle the financial crisis. All of this has convinced more than a few investors and traders that this is the time to buy riskier assets with the potential for a greater return and stock prices have been bid higher.

The important question becomes, "Is this a sucker rally with lower lows ahead, or is this an enduring new bull market?"

That is the question that some people have been asking over the last few weeks. However, with each passing day of stock market gains, fewer and fewer people seem to wonder about it, opting instead to go with the flow, to add to the momentum.

In my view, recent lows for U.S. stocks are likely to be retested again this year, probably making new lows in the process, and equity markets around the world will likely move down with them.

It really boils down to two factors - the U.S. economy and corporate earnings.

The question of decoupling - the idea that emerging markets can ignore recessions in developed economies such as the U.S., Europe, and Japan - will be addressed in a subsequent update as it is deserving of its own lengthy consideration. There is more and more promise that growth in China, Brazil, India, and elsewhere can continue despite continuing troubles in developed nations and this is a critical factor in anyone's investment approach.

For now, the discussion will be limited to the United States.

The U.S. Economy

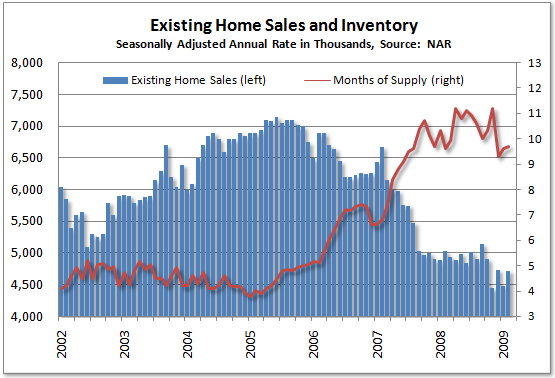

As has been the case for most of this decade, the future of the U.S. economy is dependent on housing. While financial markets and commerce may be dependent on the banking system and credit flows, the U.S. economy is soundly based on consumer spending and consumer spending, today, is driven in large part by the value of peoples' homes. Until home prices stabilize, consumers will not reemerge in big numbers to borrow and spend and, despite all the recent government initiatives, home prices are going to continue to fall this year. There is simply too much inventory in the pipeline.

As noted last week when discussing the latest report on existing home sales, it is a straightforward predicament, "the red curve and the blue bars in the nearby chart must draw much closer to each other before the downward pressure on prices abates". Despite what the NAR (National Association of Realtors) might say or what the talking heads on CNBC might offer, that is not likely to happen anytime soon as foreclosure rates continue to break records, more and more homeowners throwing in the towel, walking away from homes where they owe more than the homes are now worth. Banks continue to struggle with their growing inventory of properties and, importantly, the bulk of these bank owned properties have not yet been listed for sale.

Despite what the NAR (National Association of Realtors) might say or what the talking heads on CNBC might offer, that is not likely to happen anytime soon as foreclosure rates continue to break records, more and more homeowners throwing in the towel, walking away from homes where they owe more than the homes are now worth. Banks continue to struggle with their growing inventory of properties and, importantly, the bulk of these bank owned properties have not yet been listed for sale.

In the most recent data from both the NAR and the S&P Case-Shiller Home Price Index, home price declines continue to accelerate, largely driven by distressed property sales which, in many areas, account for more than half of all sales.

The foreclosure market is the market in many areas and defaults are now increasing fastest among prime loans made to borrowers with strong credit. The next wave of mortgage defaults will be the Alt-A and Option ARM loans where borrowers bought property with little or no documentation of income or assets, often times making only minimum payments that did not even cover all the monthly interest due. In contrast to the subprime debacle in 2007 and 2008, many of the Alt-A and Option ARM loans were used to purchase higher priced homes, a good example of this being the area where my wife and are I moving to next month - Bend, Oregon.

This is an area that, for years, has been regarded as overpriced since buyers from Portland and Seattle bid up home values earlier in the decade when the second-home buying frenzy was in full swing. In Bend, during the first quarter, notices of default almost tripled from the level of a year ago. This is in contrast to other parts of the country where foreclosure rates have leveled out at historically high levels over the last year as many of the low-priced homes with subprime mortgages have already been repossessed. Real estate prices in New York City are now starting to tumble and defaults are moving up the socio-economic ladder.

Interestingly, the expected increase in distressed sales at higher prices may have a big impact on some of the median home price statistics to be reported this year. Remember that the median price is highly dependent on the "mix" of home sales and that the sale of more higher priced homes will push up the median price even if these sales occur at steep discounts to what was paid for the same house a year or two ago. This will likely be misinterpreted as a sign of recovery.

With loan modifications souring quickly as job losses mount, housing is in no position to begin a recovery this year. While new and existing home sales may make a bottom by year-end, prices will continue to tumble and, absent any wholesale move by the government to buy up tracts of houses and bulldoze them into the ground, the supply/demand picture will not normalize until prices are much lower, probably sometime in 2010, perhaps not until 2011. Clear signs of this stabilization in prices are a prerequisite for the economy to reach a bottom and we have yet to see that.

Corporate Earnings

Reports last week indicated delinquencies increased to record highs in almost all consumer loan categories as falling home prices have now combined with job losses to create a vicious cycle downward. This only adds to the distress in the consumer sector and while both retail sales and automobile sales have shown signs of stabilizing, they remain at very low levels. Simply stabilizing at these depressed levels is not enough to support an economic rebound.

Commercial real estate defaults are now beginning to appear in large numbers, delinquent loans increasing some 41 percent from $46 billion in the fourth quarter of last year to $65 billion in the first quarter of 2009. In Los Angeles alone there are now almost $8 billion in distressed properties, nearly triple the level of late last year, and Las Vegas recently saw a 54 percent increase to $6 billion.

All of this will weigh on equity markets in the weeks and months ahead as first quarter earnings are announced.

Based on the number of warnings that have been issued thus far, bottom lines for the first quarter are likely to be almost as bad as the abysmal results seen in the fourth quarter when operating earnings for the S&P 500 overall were in the red. Importantly, there may be some big improvements in the banking sector due to "mark-to-market" changes approved last week which allow "significant" judgment in valuing assets, including mortgage-backed securities.

Total operating earnings for the S&P500 are expected to be down almost 40 percent from a year ago but it is the outlook for the future that is more important for stock prices than last quarter's results.

It will be comments by company officials about business conditions and projections of future earnings that investors will look to in order to value their shares.

Since stock prices are "forward looking" - taking into account both estimated future earnings and the health of the economy from which those earnings derive - it will be the prospects for the economy later in the year that will most influence stock prices in the near-term.

Conventional wisdom over the last fifty years or so is that, during recessions, stocks make a bottom at around the same time that monthly job losses peak and, in some cases during the second half of the 20th century, stocks put in their lows in advance of the worst of the labor market downturn. If past is precedent and if the recent January decline in nonfarm payrolls of 741,000 turns out to be the peak for this cycle, then it is reasonable to believe that the March low in equity markets could be a lasting bottom.

If past is precedent and if the recent January decline in nonfarm payrolls of 741,000 turns out to be the peak for this cycle, then it is reasonable to believe that the March low in equity markets could be a lasting bottom.

However, if either of those are untrue - that this downturn will be different than previous recessions or that job losses have not yet reached their peak - then we are more likely to see new lows sometime later this year. In my view, that is the most likely scenario - one of those two conditions will not be met.

It wouldn't be the first time that stock market investors came too early to the party.