SIFMA: US Economic Survey, End-Year 2021

Key Takeaways

- 2021 GDP growth est. +5.2%, vs. -2.3% in 2020 (median forecast, 4Q/4Q)

- 2021 unemployment rate est. 4.5%, vs. 6.8% in 2020 (4Q average)

- 2021 inflation estimate 4.9%, vs. 1.6% in 2020 (Core CPI, 4Q/4Q)

Setting the Scene

Inflation, inflation, inflation, and supply chain. Almost every conversation today involves discussing these topics. Even Fed Chair Jerome Powell said in his recent testimony to the Senate Banking Committee that it is time to retire the term transitory around inflation. As new COVID concerns and ongoing supply chain issues continue to drive inflation higher, price pressures are coming from both ends. On one hand, we are seeing demand-pull inflation, where strong demand from consumers drives up prices. We are also experiencing cost-push inflation, where supply costs – in this case driven by supply chain constraints – force prices higher.

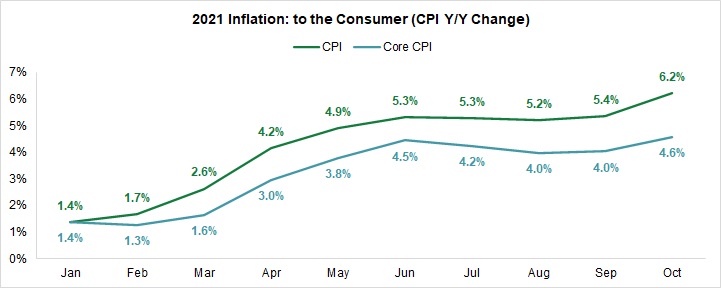

While over the summer months it looked like inflation had stabilized – in terms of growth rates remaining stable, albeit from elevated levels versus historical data – inflation spiked in October:

- Headline CPI: +6.2% Y/Y change in October, +0.8 pps from the prior month rate

- Core CPI: +4.6% Y/Y change in October, +0.6 pps from the prior month rate

The jump to current levels is certainly not the trend consumers were looking for heading into the holiday season.

The current supply chain constraints are key drivers of inflation. There are multiple levers to be fixed across the supply chain, with some taking longer to work through, such as labor shortages. Key among the supply chain issues are the delays at the Ports of Los Angeles/Long Beach (LA/LB). These ports represent nearly 40% of all containers coming in/out of the US, with volumes roughly equally split across the two. Volume at the Port of LA is holding steady: dwell time for the last 30 days for freight that is moving locally has averaged 11 days, remaining even with peak levels; on-dock rail dwell currently averages 3.5 days, well below its 13.4 day peak.

An equity research analyst covering the transportation industry noted that the “tightness will begin to structurally ease a bit as we move past peak shipping season, but given low inventory levels, will remain fairly tight well into 2022”. Our Roundtable economists estimated an easing of supply chain issues by 2Q22 (47% of responses).

2H21 Survey Results Summary

As we close out the year and head closer to the second anniversary of the COVID pandemic, some old questions linger while new ones arose in the latter half of the year. This leaves us with two main questions around the economy:

- Delta variant. Omicron variant. When will we get back to normal?

- Supply chain crunch. Strong consumer demand given the economic reopening. How long will inflation stick around and how much higher can it go?

Therefore, we asked our Roundtable of economists to provide their best assessment of the current environment and when we can approach a new normal. We also compare answers to our June survey to gauge changes in estimates of the economic outlook. We highlight the following from the survey:

Economic Forecasts

- Unemployment rate forecasted to end 2021 at +4.5%, moving to +3.8% in 2022 (4Q average)

- 2021 GDP growth expected at +5.2% (median forecast, 4Q/4Q); 2022 expected at +3.5%

- 81% of economists expect the long-term potential GDP growth rate of 1.5-2%, with 53% stating this is lower compared with pre COVID estimates

- When building their forecasts, 43% assumed a vaccine would begin to be disseminated to the broad population by 2H22

- The main factors impacting economic growth include: U.S. fiscal policy/budget, economic reopening post COVID, and U.S. monetary policy

Inflation Forecasts

- 2021 CPI – expectation +6.5% (2020 actual +1.1%)

- 2021 Core CPI – expectation +4.9% (2020 actual +1.6%)

- 67% of respondents believe current inflation pressures are transitory

- 47% of Roundtable economists expect a resolution to the supply chain constraints by 2Q22

- 60% of respondents would start to view inflation as structural versus transitory if it lasts into 2023

- 47% of respondents expect a 15% to 25% probability the U.S. will experience structurally higher inflation over the long run, followed by 27% responding 0% to 15% and 25% to 50% probability each

- Top factors to push inflation higher include: sustained breakdown of supply chains, reversal of globalization and cost increases as supply chains move back to the U.S.

- 64% of respondents believe the recently passed $1 trillion infrastructure package pose no risk to inflation

- 80% of Roundtable economists see the greater long-term risk to the economy as stagflation, given ongoing discussions around additional fiscal spending

Life After COVID-19

- 46% of respondents expect the labor force participation rate not to return to the ~63% pre-COVID average until beyond the end of 2022 and another 46% expect it to never reach pre-COVID average

- In terms of stimulus checks and enhanced unemployment benefits impacting the ability for companies to hire staff, 73% of respondents indicate that it is one of several factors

- No Roundtable economists expect another round of enhanced benefits if millions remain outside of the labor force

- 71% of respondents expect employees never to return to the office at pre-COVID levels

- The key factors listed by respondents limiting a large-scale return to office include: lingering health concerns of contracting COVID, employees choosing to continue working at home, and lack of childcare/schools closed

- Once a vaccine is distributed en masse, 47% of Roundtable economists expect consumers to approach high-density activities at increased but nowhere near pre-COVID levels while another 40% expect the activities to return to pre-COVID levels

- When gauging long lasting or permanent negative impacts from changed behaviors on the heavily COVID-impacted activities, hotels came in at the top (92% of respondents), followed by airline travel (83%) and public (67%)

- 86% of respondents believe proof of vaccination should be required for airline travel, return to office and crowded events

- Looking at COVID safety measures as a hurdle to returning to normal, 43% of respondents replied they view all requirements in aggregate as the biggest hurdle

- 58% of respondents expect us to be required to continue wearing masks through 2H22, 33% responded 1H22

- 87% believe the development of the Merck and Pfizer antiviral pills will somewhat accelerate the return to normal

Fed Actions

- Respondents indicated that should we see a reversal in the COVID recovery and therefore declining economic factors, the top tool the Fed will use will be asset purchases/balance sheet (93% of respondents) followed by communication (87%)

- As to the efficiency of the Fed’s communication with markets around its timeline for shifting monetary policy, 67% of respondents indicated it’s excellent/very clear, while 33% said murky but decipherable

- Roundtable economists remain divided on when the Fed will begin to lift its target range for the federal funds rate with 29% each responding 2Q22, 3Q22, and 4Q22

- The factors listed as most important to the Fed’s rate decision were: inflation pressure/expectations, resumption of real economic activity, and COVID impact on labor conditions

Fiscal Stimulus and Tax Policy

- 33% of respondents expect the President’s $1 trillion hard infrastructure package to increase 2022 GDP estimates by 0-10 bps

- 100% of Roundtable economists expect the proposed human infrastructure plan will be passed; all believe the final package will be $1-2 trillion

- 30% of respondents expect the President’s $1.75 trillion human infrastructure package to increase 2022 GDP estimates by 10-20 bps and another 30% expect increase of 20-30 bps

- 85% of respondents view the bigger risk to the economy is the government doing too much, therefore the economy overheats

- When considering additional stimulus, 54% respondents indicated government should consider the debt burden as a further rise could impeded long-term growth or incite inflation

Trade Policy

- 29% of Roundtable economists expect the U.S. to renew suspensions on tariffs with the EU and expand the list of goods and 29% indicated it’s too early to tell

- 57% of Roundtable economists expect the U.S. to address perceived unfair trade practices by China by only monitoring the situation, with 29% expecting the tariffs to be removed on some goods

- When asked if the negative sentiments around China’s handling of COVID will have a lasting impact on trade relations with China, 57% responded yes

- In light of this, 36% of respondents expect a meaningful shift to domestic production, thereby reducing U.S. reliance on overseas production