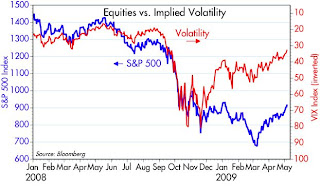

This has been a theme here for a long time, and it's playing out nicely after having derailed a bit in February and early March. The VIX index, a measure of both fear and the underlying volatility of stock prices, has declined significantly from its highs of last year, and now we see that equity prices have moved back up from their lows.

This has been a theme here for a long time, and it's playing out nicely after having derailed a bit in February and early March. The VIX index, a measure of both fear and the underlying volatility of stock prices, has declined significantly from its highs of last year, and now we see that equity prices have moved back up from their lows.This is the sort of thing that can feed on itself. This whole crisis was accentuated, if not precipitated, by fear—fear of a collapse in the banking system, fear of a global depression, fear of deflation. Fear caused consumption expenditures to hit an air pocket; fear caused people to mistrust counterparties, to deleverage, and to build up their stores of cash.

Now that is reversing, and that means that money can start flowing again (i.e., the velocity of money can pick back up). That will support stronger spending, more investment, and potentially, higher prices. Very bullish, given the extremely depressed level of valuations that prevailed not too long ago. All it took to produce a strong rally was the realization that the economy was not going down a black hole, as so many doomsayers were predicting.

I first posted this chart last December, when I noted that declining swap spreads were an excellent sign that the fixed-income market was recovering, and that presaged improvement in other areas as well. Swap spreads have since gone on to tighten further, yesterday falling below 50 bps.

I first posted this chart last December, when I noted that declining swap spreads were an excellent sign that the fixed-income market was recovering, and that presaged improvement in other areas as well. Swap spreads have since gone on to tighten further, yesterday falling below 50 bps.It may be too much to hope that equities close the gap with swap spreads depicted on this chart any time soon, but at the very least I think this tells us that the equity rally is not ephemeral and has excellent upside potential.

The Challenger, Gray & Christmas tally of corporate layoff announcements in April dropped again, for the third straight month. Additionally, the ADP measure of job losses came in about 25% below expectations, suggesting that Friday's jobs number could be significantly better than expected, perhaps showing losses of only 500-550K instead of the expected 635K. The market's rally is supported by clear signs of improving economic fundamentals.

The Challenger, Gray & Christmas tally of corporate layoff announcements in April dropped again, for the third straight month. Additionally, the ADP measure of job losses came in about 25% below expectations, suggesting that Friday's jobs number could be significantly better than expected, perhaps showing losses of only 500-550K instead of the expected 635K. The market's rally is supported by clear signs of improving economic fundamentals.